In the rapidly evolving landscape of fast-moving consumer goods (FMCG), the battle for shelf space has migrated from the physical aisle to the digital ecosystem. Pilgrim’s Europe, the powerhouse behind the iconic Richmond sausage brand, currently finds itself at the forefront of this shift. The company is midway through a comprehensive, multi-channel awareness campaign designed to cement its market position. By deploying a sophisticated mix of linear television, video on-demand (VOD), paid social media, out-of-home (OOH) advertising, and a strategic infusion of retail media, Pilgrim’s is attempting to redefine how high-penetration food brands maintain visibility in a fragmented media environment.

However, the Richmond campaign serves as a microcosm of a much larger, more complex struggle. As European and British brands attempt to mirror the retail media maturity of their American counterparts, they are finding that the infrastructure, organizational culture, and measurement standards of the industry are still catching up to the ambitions of global marketers.

The State of Play: A Rapidly Maturing Market

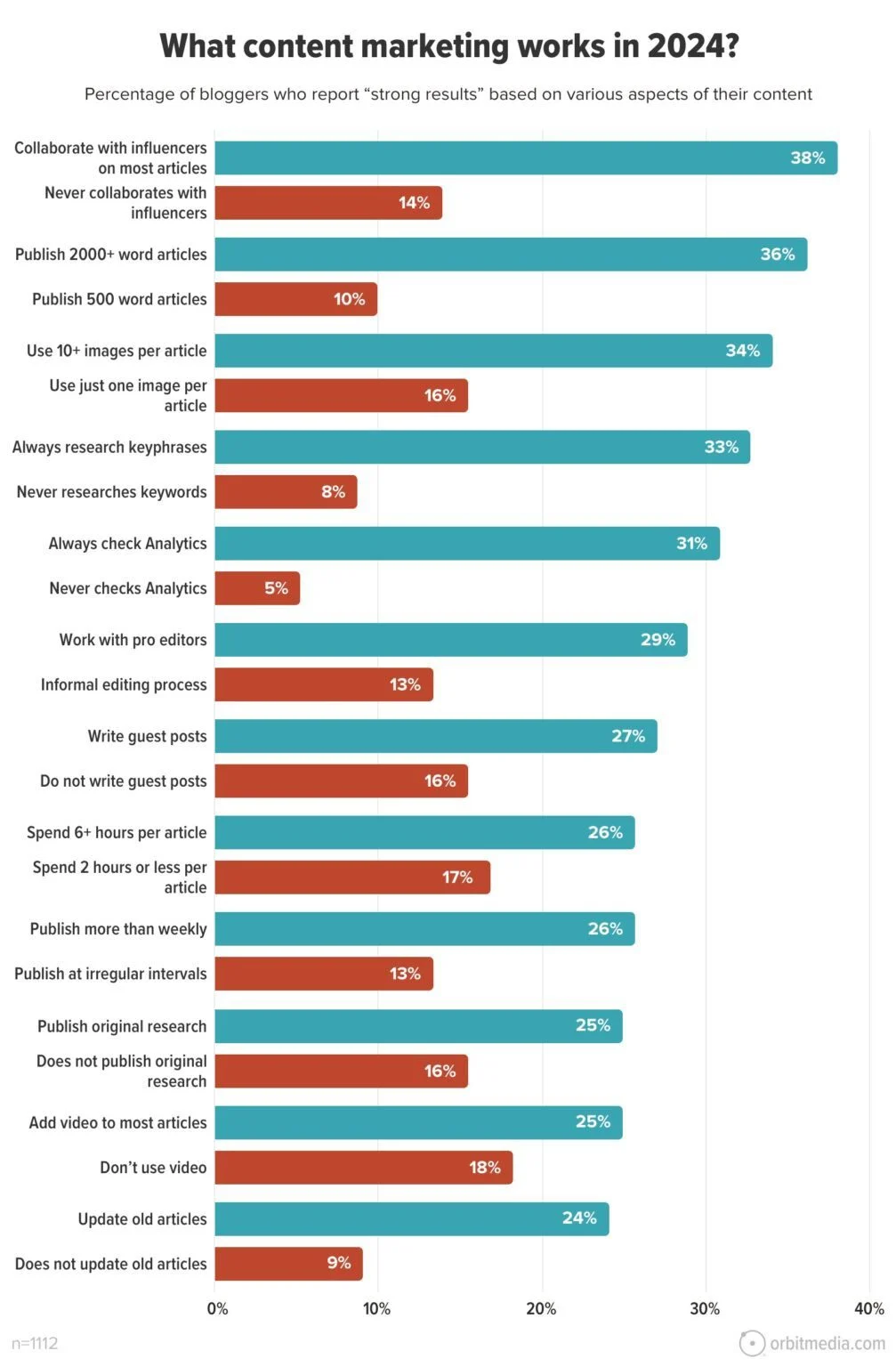

According to data from AA/WARC, retail media in the U.K. is experiencing a period of explosive growth. In 2025 alone, the sector grew by 17.5% year-on-year, reaching a valuation of £3.7 billion. This figure represents nearly 10% of the U.K.’s total £40 billion digital advertising market, positioning retail media as the third fastest-growing channel in the country, trailing only social media and addressable TV.

Yet, despite this momentum, the U.K. market remains in a formative stage. While the United States boasts over 250 operational retail media networks (RMNs), the U.K. landscape is far more concentrated, with roughly 28 major networks. Leading this charge are the "Big Four" grocers—Tesco, Sainsbury’s, Asda, and Morrisons—alongside specialized entities like the pharmacy chain Boots. In continental Europe, retail giants like Carrefour are mirroring these developments, yet the billion-dollar gap in investment volume compared to the U.S. highlights a significant disparity in both scale and complexity.

The Richmond Strategy: Balancing Tradition and Innovation

For Chris Doe, FMCG marketing director at Pilgrim’s, the challenge of the Richmond campaign is rooted in the unique nature of the product. "Richmond is a high-penetration category," Doe explains. "The aisle we operate in has high footfall, so the challenge isn’t just awareness; it’s how you stand out in the shopper journey."

Consequently, the Pilgrim’s strategy is heavily weighted toward classic shopper marketing—in-store displays and digital search inventory. While these are traditional tactics, they are being deployed within the retail media networks of Tesco, Asda, Sainsbury’s, and Morrisons to ensure that the brand remains the primary choice for the consumer at the point of decision. This approach highlights a central tension in the industry: the preference for conversion-focused activations over the off-site, upper-funnel targeting that characterizes the more advanced American retail media model.

Chronology of a Shift: The Rise of the "Full-Funnel" Ambition

For years, retail media was viewed by many brands as a "trade" activity—a cost of doing business to secure shelf space. The following timeline tracks the industry’s transition toward a more strategic, marketing-led function:

- 2020–2022: The "Pandemic Acceleration." The sudden surge in e-commerce forced retailers to recognize their websites as premium advertising real estate, leading to the formalization of internal retail media divisions.

- 2023: The "Standardization Struggle." As ad budgets shifted, brands began demanding better measurement. Retailers began investing in first-party data (Tesco’s Clubcard, Sainsbury’s Nectar) to prove ROI.

- 2024: The "Video Invasion." Recognizing that search alone could not capture brand-building budgets, major retailers began launching premium video ad formats across their apps and websites.

- 2025: The "Structural Integration." Major FMCG firms began dissolving the silos between sales and marketing teams to create a unified approach to retail media spend.

The Amazon Factor and the War for Ad Dollars

It is impossible to discuss the U.K. retail media market without acknowledging the dominant force of Amazon. Holding an estimated 73% share of retail media spending in the U.K., Amazon is effectively the primary architect of the market. As Alex Walker, managing director at Havas Market UK, succinctly puts it, "Amazon drives the market."

Amazon’s influence has forced grocers to innovate rapidly. By enabling advertisers to target Netflix media buys using commerce data via its DSP (Demand-Side Platform), Amazon has successfully moved into the realm of upper-funnel brand advertising. This has created a "price war" of sorts. Jess Haley, managing director, EMEA at Kepler, notes that platform competition is pushing brands to increase their spending by 30–40% annually. "Amazon reps are emphasizing video inventory in pitches, and the higher price of that inventory—often arranged through private marketplace (PMP) deals—is a primary factor in the rising cost of retail media," Haley notes.

Tesco has responded in kind. In April, the grocer launched premium video ad formats across its app and website, claiming an audience reach of 12 million shoppers. Nick Ashley, propositions and go-to-market director at Tesco Media, frames this as a bridge between inspiration and action: "We think it’s an opportunity for top-of-funnel media to turn the inspiration mindset into an immediate, measurable outcome." The strategy is paying off; Tesco saw a 24% year-on-year rise in campaigns last year, with 91% of participating brands increasing their spend.

Implications: The Problem of "Disconnected Commerce"

Despite the growth in inventory, a significant hurdle remains: what industry experts call "disconnected commerce." This refers to the persistent divide between the sales teams, who manage trade relationships with retailers, and the marketing departments, who control the digital media budget.

Ian Black, head of retail media at Publicis, argues that this disconnect has allowed retailers to exert undue leverage in trade negotiations, sometimes making brands feel "strong-armed" into media investments. However, the industry is beginning to pivot. Sharon Palmer, director of group accounts at IDHL, observes that control is finally shifting away from sales and into the hands of marketing teams.

"Big brands in CPG, beauty, and pharma are strategically shifting and restructuring to combine the powers of both teams," says Black. By treating retail media as a cohesive part of the brand’s total media investment—rather than a secondary trade cost—brands are beginning to demand more from retailers.

The Path Forward: Standardization and Self-Service

If retail media is to become a legitimate rival to traditional digital channels like Google or Meta, it must solve three critical issues:

- Self-Service Capabilities: Media agencies need direct access to platforms to optimize campaigns in real-time. While Tesco and Sainsbury’s have made strides, agencies argue that finer control over measurement and planning is still lacking.

- Standardized Measurement: The lack of a unified measurement framework across the 28+ networks in the U.K. is a major point of friction. As Havas’s Alex Walker notes, the current situation is "quite a heavy lift" for marketers trying to reconcile data across multiple platforms.

- Proof of Full-Funnel Impact: Kavita Cariapa, head of commerce media, EMEA at Dentsu, warns that retail media networks haven’t yet proven their worth beyond conversion-led activations. For brands to shift more of their upper-funnel budget into these channels, retailers must demonstrate that their networks can do more than just facilitate a transaction—they must prove they can build a brand.

Conclusion: The Maturity Mandate

The journey of Richmond and its peers reflects a broader realization: retail media is no longer a peripheral experiment; it is the new battleground for consumer attention. However, the current "disconnected" nature of the industry is unsustainable.

For the U.K. market to reach its full potential, retailers must shift their focus from merely selling inventory to providing a seamless, transparent, and standardized ecosystem. Until then, brands will continue to treat retail media as a conversion lever rather than a holistic growth engine. The retailers that win in the next decade will not necessarily be the ones with the most traffic, but the ones that empower marketers to align their trade and media strategies into one, unified, and measurable force.