The landscape of artificial intelligence infrastructure is undergoing a seismic shift, characterized not only by exponential leaps in computational power but by equally staggering escalations in capital expenditure. As Nvidia continues to solidify its dominance as the architect of the modern AI economy, its latest data center platform—the Vera Rubin superchip—has emerged as a focal point of both technological awe and financial disbelief.

New estimates from a Morgan Stanley research report have cast a revealing, if not sobering, light on the costs associated with deploying this cutting-edge hardware. The figures suggest that a single VR200 NVL72 rack—the building block for the next generation of hyperscale AI data centers—carries a staggering price tag of approximately $7.8 million. This valuation underscores a reality that industry insiders have long whispered: the "AI gold rush" is increasingly becoming a game reserved for the wealthiest corporations on the planet.

The Anatomy of a $7.8 Million Investment

To understand the scale of this investment, one must look at the Bill of Materials (BOM) breakdown provided by financial analysts. According to the report, of the $7,803,148 estimated cost for a single NVL72 rack, a massive $2,001,600 is attributed solely to memory components.

This represents a staggering 435% increase in memory expenditure compared to the previous-generation GB300 systems. This surge is driven by the insatiable demand for high-bandwidth memory (HBM) and advanced DDR5 modules required to feed the six-trillion-transistor behemoths that power the Rubin architecture. While these figures represent the estimated cost for cloud service providers (CSPs) rather than Nvidia’s internal production costs, they offer a stark look at the "Nvidia premium" and the sheer complexity of modern supply chain economics.

Chronology of the AI Hardware Arms Race

The ascent to the Vera Rubin era did not happen in a vacuum. It is the culmination of a decade-long acceleration in semiconductor design, specifically tailored for the massive parallel processing requirements of Large Language Models (LLMs).

- 2022–2023 (The H100 Era): Nvidia’s Hopper architecture established the baseline for the modern AI data center, creating a global shortage as every major tech firm scrambled to secure capacity.

- Early 2026 (The Blackwell Pivot): Nvidia introduced the Grace Blackwell architecture. Even before its official market saturation, the demand for Blackwell GPUs exceeded expectations, signaling a move toward integrated superchips rather than discrete components.

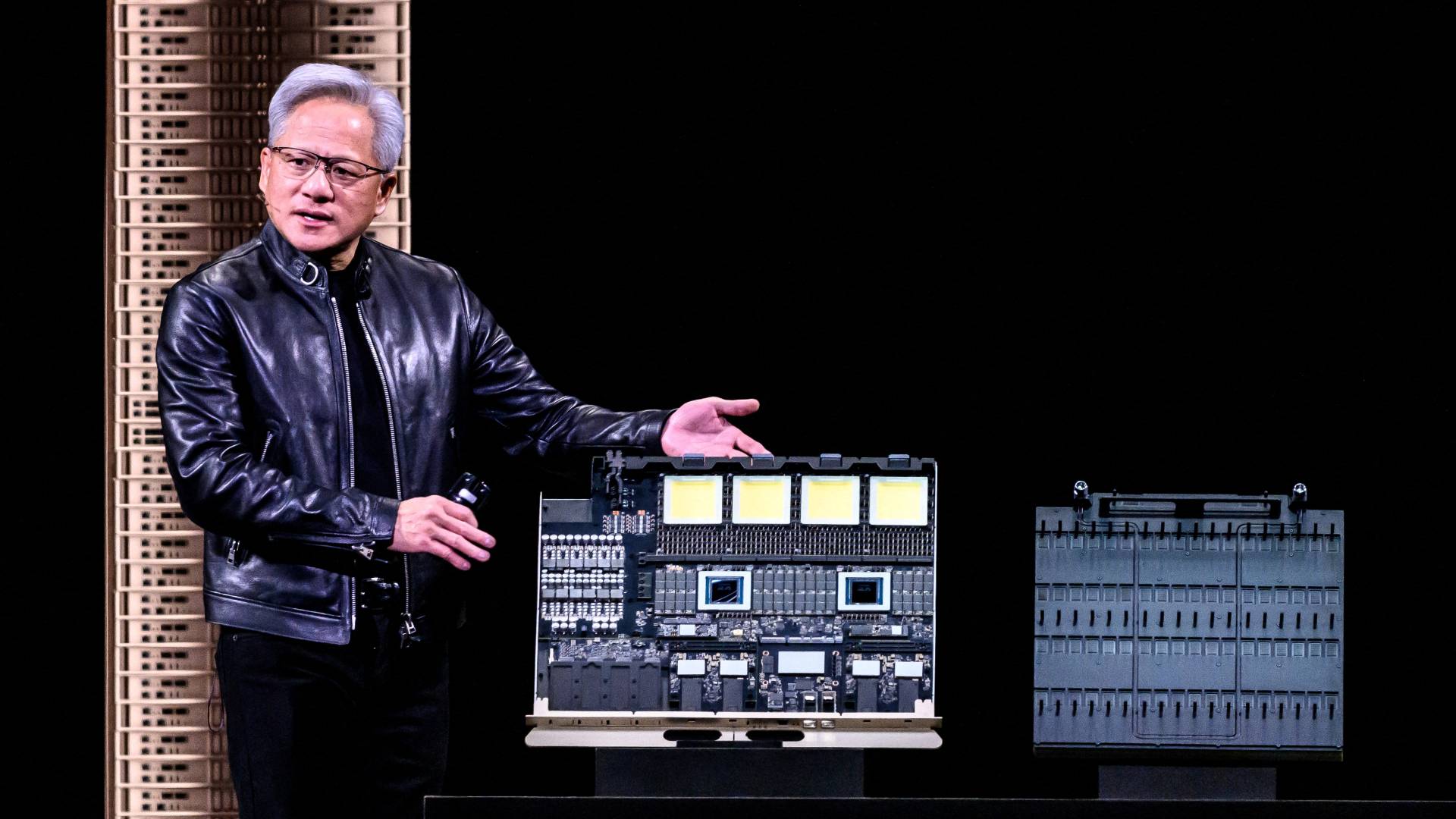

- Mid-2026 (The Rubin Unveiling): At the GTC 2026 keynote, CEO Jensen Huang took the stage to announce the Vera Rubin platform. Described as a generational leap in AI GPU architecture, Rubin was designed to handle the next frontier of "frontier models"—the massive neural networks that require trillions of parameters.

- Present Day: Industry analysts are now conducting the first deep-dive cost analyses (such as the Morgan Stanley report), revealing the fiscal reality of adopting this next-generation infrastructure.

Supporting Data: Why the Costs are Skyrocketing

The financial burden of the Vera Rubin platform is not merely the result of "Nvidia’s greed," as some industry critics might suggest. It is the result of fundamental changes in hardware physics and manufacturing complexity.

1. The Transistor Density Gap

The Vera Rubin superchip boasts an unprecedented six trillion transistors. By comparison, the upcoming RTX 5090—a titan of the consumer gaming market—is expected to utilize around 92 billion transistors. The R&D costs to design a chip of this density, combined with the extreme yield risks at the foundry level (TSMC’s latest process nodes), create a massive baseline cost that must be amortized across fewer, albeit more powerful, units.

2. The Memory Bottleneck

The "memory crisis" mentioned by former Samsung executives is a primary driver of the $2 million memory bill per rack. Because AI models are memory-bound, Nvidia is forced to integrate increasingly faster and larger pools of HBM. This creates a supply-demand imbalance:

- Competition for Wafers: AI chips compete for the same advanced manufacturing capacity as consumer electronics, but because the profit margins for AI chips are exponentially higher, memory manufacturers are prioritizing server-grade silicon, driving up prices for everyone else.

- Specialized Packaging: Unlike standard consumer RAM, HBM requires sophisticated 2.5D or 3D stacking techniques, which significantly complicates the assembly process and increases the probability of component failure, thereby inflating the final price.

Official Responses and Strategic Outlook

Nvidia has remained characteristically bullish regarding the cost-to-performance ratio of its new hardware. During the Q1 2026 earnings call, where the company reported a historic $81.6 billion in quarterly revenue, CEO Jensen Huang defended the trajectory of his hardware.

"Every single frontier model company will jump on Vera Rubin from the get-go," Huang stated in response to investor inquiries. He emphasized that the transition to Rubin is fundamentally different from the transition to Blackwell. While Blackwell was a successful iteration, Rubin is being treated as an essential utility for companies aiming to remain competitive in the AGI (Artificial General Intelligence) race.

From Nvidia’s perspective, the $7.8 million price tag is not a barrier; it is a value proposition. If a company spends nearly $8 million on a rack, they are gaining the ability to train models that were previously thought to be impossible to compute within a reasonable timeframe. For the giants of the industry—Microsoft, Meta, Google, and Amazon—this cost is viewed as a necessary capital expenditure to secure their future in the AI-centric global market.

Broader Implications: A Filter for the Tech Sector

The economic weight of the Vera Rubin platform has profound implications for the wider technology landscape:

The "AI Divide"

As the cost of infrastructure climbs, the barriers to entry for AI development are becoming insurmountable for all but the largest enterprises. We are witnessing the birth of an "AI Divide," where the top-tier tech firms possess the compute power to develop frontier models, while startups and mid-sized enterprises are relegated to leasing access to that compute at significant premiums.

The Impact on Consumer Hardware

The ripple effect of AI demand on the consumer market is unavoidable. As long as the data center remains the most profitable sector for silicon manufacturers, the supply of memory and logic components for gaming PCs and consumer laptops will remain tight. The $300 price tag for a high-end 32GB DDR5 kit, which once seemed like an anomaly, may well become the new floor as memory manufacturers focus their capacity on high-margin enterprise products.

Market Consolidation

The massive profitability of Nvidia’s data center division serves as both a boon and a potential risk. While it provides the capital necessary for unprecedented R&D, it also centralizes the power of the global AI infrastructure in a single company. This concentration of control over the "picks and shovels" of the AI revolution makes the global tech economy uniquely sensitive to Nvidia’s production cycles and pricing strategies.

Conclusion: The Price of Innovation

The report from Morgan Stanley serves as a reality check for an industry blinded by the glittering potential of generative AI. While the Vera Rubin platform represents a masterclass in engineering, it is also a testament to the fact that the future of computing will be exceptionally expensive.

For the average observer, the $7.8 million price tag for a single rack of hardware is an abstract number—a figure so large it defies typical consumer logic. Yet, in the context of the AI arms race, it is merely the entry fee. As we look toward the latter half of the decade, the question remains: will the productivity gains promised by these massive investments eventually justify their cost, or are we witnessing the formation of a capital-intensive bubble that will eventually force a correction in the tech sector? For now, Nvidia continues to dictate the terms of the market, and the world’s most powerful companies are more than willing to pay the price.