The global mobile gaming landscape experienced a period of significant volatility and strategic realignment throughout June 2026. As the industry navigates a post-pandemic growth stabilization phase, the battle for user acquisition and monetization remains as fierce as ever. According to the latest data provided by AppMagic, the month of June served as a watershed moment for several major players, marked by the dramatic displacement of long-standing download leaders and the continued dominance of industry giants in the revenue sector.

Main Facts: A Shift in the Guard

The most striking headline for June 2026 is the total upheaval of the mobile download charts. Easybrain has officially ascended to the top of the leaderboard, capturing a staggering 112.7 million downloads. This victory is particularly notable as it marks the end of an era for Miniclip, which, despite its historical status as the gold standard for high-volume casual gaming, failed to secure a position within the Top 15 this month.

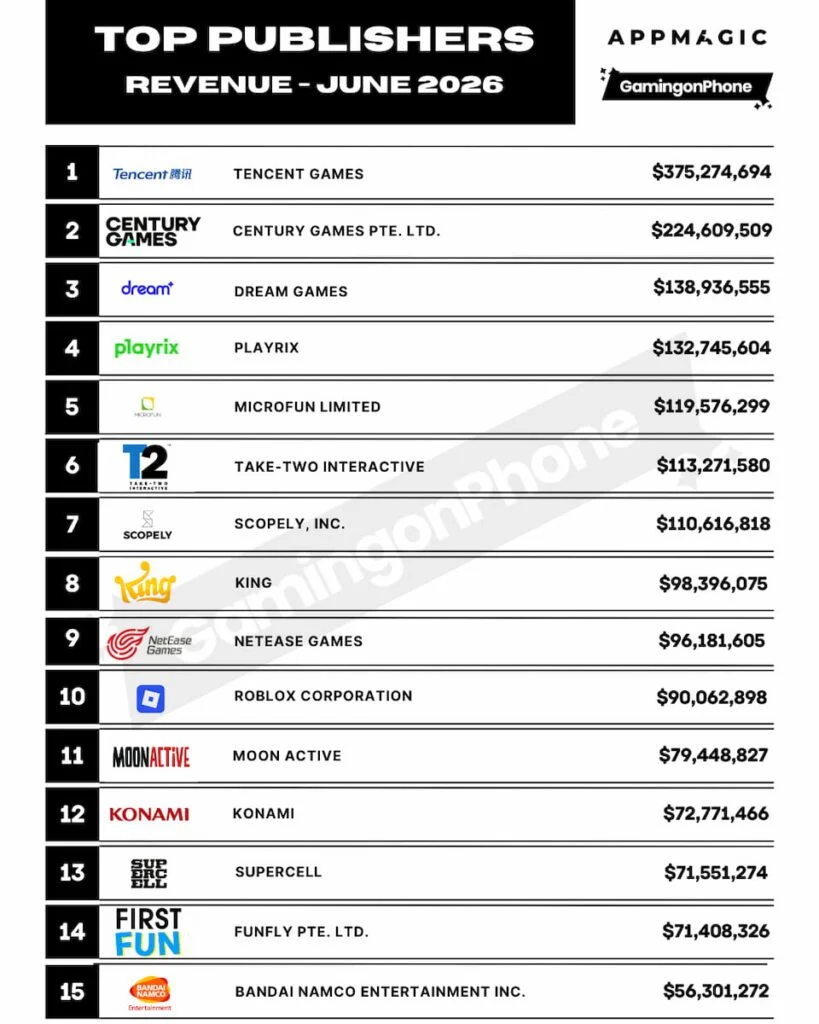

Conversely, the revenue sector remains a bastion of stability. Tencent Games maintains its iron grip on the top spot, demonstrating the immense staying power of its flagship titles, Honor of Kings and PUBG Mobile. While the download charts are subject to the fickle nature of viral trends and hyper-casual surges, the revenue charts reflect the long-term loyalty and monetization efficiency that only massive, ecosystem-based publishers can command.

Chronology of Market Movements: June 2026

To understand the current state of the market, one must look at the trajectory of the top publishers over the last 30 days.

The Rise of Easybrain and the Hyper-Casual Shuffle

Early June saw a concentrated push by Easybrain to maximize its market share, successfully leveraging its puzzle-centric portfolio to overtake the competition. Following them, Azur Games and VOODOO remained in a tight formation at second and third place, respectively. Azur Games recorded 69 million downloads, while VOODOO trailed by a razor-thin margin at 68.7 million.

The mid-month analysis showed Learnings gaining significant momentum, climbing to fourth place (67.7 million downloads) as it capitalized on changing consumer preferences. Outfit7, the developer behind the iconic Talking Tom and Talking Angela franchises, climbed to fifth place (51.9 million downloads), buoyed by successful content updates such as the "Spooky Quest" for My Talking Tom 2 and the "Nail Salon" feature in My Talking Angela 2.

Mid-Month Revenue Consolidation

By the third week of June, revenue trends began to solidify. Tencent Games, holding steady at $375.3 million in monthly revenue, faced little challenge from the rest of the field. The mid-tier of the revenue chart saw a noteworthy shift as Scopely outperformed King, moving into seventh place with $110.6 million. This move pushed the Candy Crush creator down to eighth place with $98.4 million, underscoring the success of Scopely’s aggressive live-ops strategy.

Supporting Data: By the Numbers

The following tables synthesize the performance data for the top publishers during the June 2026 cycle.

Top 15 Mobile Game Publishers by Downloads

| Rank | Publisher | Downloads (Approx.) |

|---|---|---|

| 1 | Easybrain | 112.7 Million |

| 2 | Azur Games | 69.0 Million |

| 3 | VOODOO | 68.7 Million |

| 4 | Learnings | 67.7 Million |

| 5 | Outfit7 | 51.9 Million |

| 6 | SayGames Ltd | 50.7 Million |

| 7 | BabyBus | 48.4 Million |

| 8 | Supercent | 36.2 Million |

| 9 | CrazyLabs | 33.8 Million |

| 10 | IVYMOBILE | 30.6 Million |

(Note: Positions 11–15 include returning players such as Garena International, spurred by the resurgence of Free Fire MAX, as well as Tencent and Supersonic Studios.)

Top 15 Mobile Game Publishers by Revenue

| Rank | Publisher | Revenue (Approx.) |

|---|---|---|

| 1 | Tencent Games | $375.3 Million |

| 2 | Century Games | $224.6 Million |

| 3 | Dream Games | $138.9 Million |

| 4 | Playrix | $132.7 Million |

| 5 | Microfun Limited | $119.6 Million |

| 6 | Take-Two Interactive | $113.3 Million |

| 7 | Scopely | $110.6 Million |

| 8 | King | $98.4 Million |

| 9 | NetEase Games | $96.2 Million |

| 10 | Roblox Corporation | $90.1 Million |

Official Responses and Strategic Commentary

While many publishers keep their internal analytics private, the movements seen in June align with broader industry trends discussed in recent developer conferences.

Outfit7’s performance in June is a case study in effective live-ops. By introducing deep customization features, such as the "Nail Salon" in My Talking Angela 2, the publisher has successfully increased the lifetime value and engagement duration of its existing user base. This strategy of "re-engaging the core" is a recurring theme among the top 10 revenue generators.

Conversely, the decline of companies like SayGames Ltd—which slipped from fourth to sixth place—illustrates the difficulty of maintaining high download volumes in the hyper-casual market. As user acquisition costs (UA) rise, publishers are forced to rotate titles faster, often leading to temporary dips when a flagship title loses its viral momentum.

Implications for the Future of Mobile Gaming

The June 2026 data provides a clear roadmap for what investors and stakeholders should expect in the coming quarter.

1. The Death of "Static" Dominance

The sudden absence of Miniclip from the top 15 download rankings serves as a warning: no publisher is too large to fail in the hyper-casual space. The market is becoming increasingly volatile, where success is tethered to the ability to launch or refresh titles that resonate with Gen Alpha and Gen Z audiences.

2. Revenue Stability vs. User Acquisition

We are seeing a growing divergence between the "Download Kings" and the "Revenue Kings." The top of the download charts is occupied by companies focusing on mass-market reach and ad-supported models. In contrast, the top of the revenue charts is occupied by companies focusing on deep meta-layers, social connectivity, and IAP (In-App Purchase) heavy loops.

3. The "HoYoverse" Departure

The fact that HoYoverse dropped out of the top 15 revenue list this month is a significant signal. It suggests that, without a major content drop or a new title launch, even the most successful Gacha-based publishers can see their monthly revenue fluctuate significantly. This highlights the "event-driven" nature of the modern mobile economy.

4. Resurgence of Battle Royales

The return of Garena International to the download charts, specifically driven by Free Fire MAX, signals that the "Battle Royale" genre is far from dead. Despite market saturation, core gameplay loops that provide high-octane, competitive social experiences continue to draw millions of new users, provided the publisher can optimize for lower-end devices.

Conclusion

June 2026 has been a month of transition. As we move into the second half of the year, the industry is clearly pivoting toward more sustainable, long-term engagement strategies. While Easybrain enjoys its moment in the sun at the top of the download charts, the steady, consistent performance of Tencent and Century Games proves that monetization remains the true anchor of the industry.

For developers looking to break into the top 15, the lesson of June is clear: innovation in gameplay features—as seen with Outfit7—is the only way to insulate oneself from the volatility of the download market. As we look toward July, all eyes will be on whether the current leaders can maintain their momentum or if the market will once again undergo a radical reshuffling.

For ongoing analysis of the mobile gaming market, including deep dives into publisher strategies and industry-wide trends, stay tuned to our regular reports. Join our official WhatsApp Channel, Telegram Group, or Discord server for the most up-to-date information.