Snap Inc., the parent organization behind the ubiquitous social media platform Snapchat, has officially released its Q1 2026 earnings report, painting a portrait of a company caught in a precarious balancing act. While the topline figures suggest modest growth, a deeper examination of the geographic breakdown and regulatory headwinds reveals significant structural challenges. CEO Evan Spiegel has characterized this period as a "crucible moment" for the firm, as it attempts to maintain its relevance in an increasingly saturated and heavily regulated digital landscape.

Main Facts: The State of the Snap Ecosystem

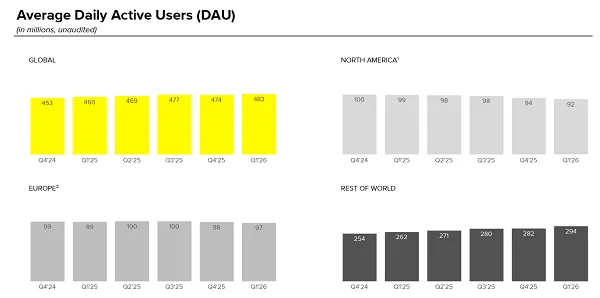

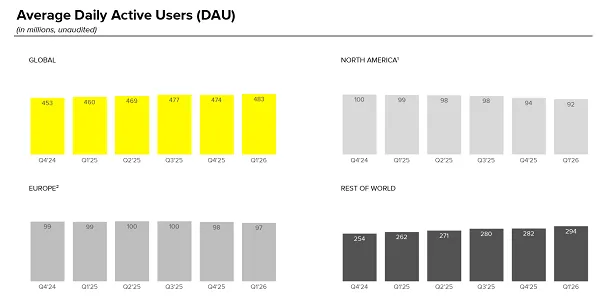

The primary takeaway from the Q1 2026 filing is a tale of two realities: global expansion and domestic contraction. Snapchat reported an addition of 9 million daily active users (DAU) over its Q4 2025 figures, bringing the total platform-wide count to 483 million. On the surface, this represents a resilient recovery, particularly when contrasted with the loss of 3 million users witnessed in the previous reporting period.

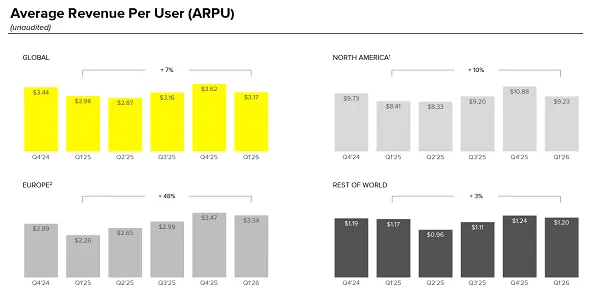

However, the revenue engine—which remains heavily reliant on the North American and European markets—is showing signs of fatigue. In North America, the platform’s most lucrative territory, usage declined by 2 million, sliding to 92 million DAU. Similarly, the European market saw a contraction of 1 million users. The critical implication here is that the entirety of Snap’s growth is currently being sourced from developing regions where the company has yet to mature its business tools or maximize Average Revenue Per User (ARPU). Consequently, while the user base is technically expanding, the platform’s capacity to monetize that growth is fundamentally constrained.

Chronology of Challenges: From Growth to Consolidation

The trajectory of Snap over the last several quarters suggests a pivot from the "growth at all costs" mentality toward a focus on fiscal discipline and existential survival.

- Late 2025: Snap faced a turbulent Q4, resulting in a net loss of 3 million users and prompting a strategic reassessment of its overhead costs.

- February 2026: The company faced a significant regulatory blow in Australia, where new social media age-restriction laws forced the platform to disable or lock approximately 415,000 teen accounts. This served as a "canary in the coal mine" for the potential impact of similar legislation pending in the UK, Germany, and Spain.

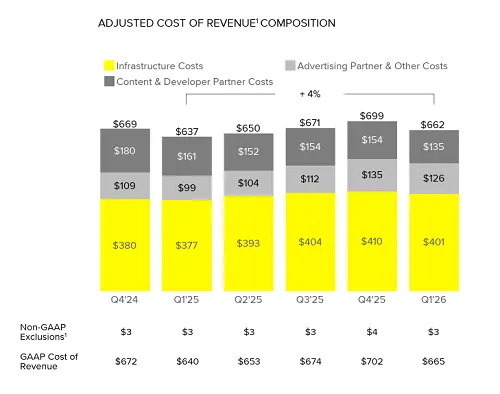

- April 2026: Snap released its Q1 2026 earnings, reporting $1.53 million in quarterly revenue—a 12% year-over-year increase—yet tempering the optimism with an admission of declining engagement in its core Western markets.

- Present Day: The company is currently engaged in an aggressive cost-cutting campaign, including a 16% reduction in its full-time workforce, as it pivots toward the upcoming launch of its proprietary AR hardware.

Supporting Data: The Monetization Gap

The disparity between user growth and revenue generation is perhaps best illustrated by the company’s regional performance data. While the platform boasts 956 million monthly active users (MAU), the revenue per user in non-Western markets remains significantly lower than in the U.S. and Canada.

Snap’s ad business, however, has shown surprising resilience. The company reported that "Sponsored Snaps" are driving meaningful performance, while Dynamic Product Ads grew by over 30% year-over-year. The strength in the Small and Medium-sized Business (SMB) sector suggests that Snap’s advertising tools are becoming more accessible to a broader range of brands. Yet, there is a looming concern regarding "ad fatigue." As the company attempts to bolster revenue by integrating more ads into user direct messages and other intimate digital spaces, it risks eroding the very "connective experience" that attracts its core demographic in the first place.

Official Responses and Strategic Outlook

In his latest investor update, CEO Evan Spiegel emphasized that the company is at a critical juncture. The strategy moving forward relies on three pillars: diversifying ad revenue, increasing the efficiency of the core application, and a high-stakes gamble on Augmented Reality (AR) hardware.

Snap has consistently maintained that its focus remains on "innovative engagement." However, critics point out that the company’s product roadmap has been largely iterative rather than transformative. The introduction of "Spotlight," while successful, was widely viewed as a direct response to the market dominance of TikTok. Furthermore, the company’s push into subscription services, specifically "Snapchat+," provides a steady stream of recurring revenue but remains a drop in the bucket compared to the scale of its advertising intake.

Implications: The Regulatory and Competitive Landscape

The most significant external threat to Snap’s long-term viability is the global legislative shift regarding social media and minors. The Australian precedent of banning users under 16 is gaining traction globally. Given that a substantial portion of Snapchat’s user base falls within the teen demographic, the potential for a "domino effect" in larger European economies—such as Germany and the UK—poses a existential threat to the platform’s user growth trajectory.

Moreover, the competitive landscape is tightening. Snap is not merely competing with legacy giants like Meta; it is also fighting to maintain relevance among younger demographics who are increasingly splitting their time between a fragmented array of niche platforms and generative AI-driven tools.

The AR Gamble

Perhaps the most speculative element of Snap’s future is its upcoming AR glasses. While the company has long positioned itself as an "AR-first" tech firm, the hardware industry is unforgiving. Early reports and prototypes suggest that Snap’s upcoming device may struggle to compete with the sleek, AI-integrated wearables currently being pioneered by Meta. With Meta rumored to launch a more advanced, consumer-friendly AR solution in 2027, the window for Snap to establish a hardware footprint is rapidly closing.

Market Capitalization and the "Demographic Ceiling"

Perhaps the most damning observation regarding Snap’s current state is its difficulty in retaining users as they age. Snapchat has historically struggled to remain a "critical" app for users once they exit their early twenties. This demographic ceiling inherently limits the company’s total addressable market and, by extension, its market capitalization. Without a clear strategy to transition its user base into older life stages—or to consistently capture the next generation of digital natives—Snap’s growth will likely remain bounded by these demographic shifts.

Conclusion: A Pivot or a Plateau?

As we move further into 2026, the data indicates that Snap Inc. is in a state of managed decline in its core markets, offset by successful but lower-margin growth elsewhere. The company’s ability to survive this "crucible moment" depends less on its ability to acquire new users and more on its ability to squeeze higher value from the existing base without triggering an exodus of its disillusioned youth audience.

The path forward for Evan Spiegel is narrow. To succeed, the company must successfully navigate the complex regulatory waters of Europe and North America, prove that its AR hardware can find a market niche against tech behemoths, and fundamentally rethink its user retention strategy. If it fails, Snap risks being relegated from a primary social hub to a secondary, legacy platform—a cautionary tale of the ephemeral nature of social media dominance.

Investors and users alike will be watching closely as the next two quarters unfold. Whether this represents a successful pivot to a leaner, more diversified business model or the beginning of a long-term plateau will be the defining narrative of Snap’s fiscal year.