By Ronan Shields | May 14, 2026

As the dust settles on the Q1 2026 earnings season, the advertising technology sector finds itself at a precarious crossroads. While the industry is collectively pivoting toward an "agentic" future fueled by artificial intelligence, the actual financial performance of the sector remains a study in contrasts. From the meteoric rise of AppLovin to the unexpected softening of giants like The Trade Desk, the last two weeks of reporting have laid bare the tensions between technological promise and operational reality.

The State of the Industry: A Broad Overview

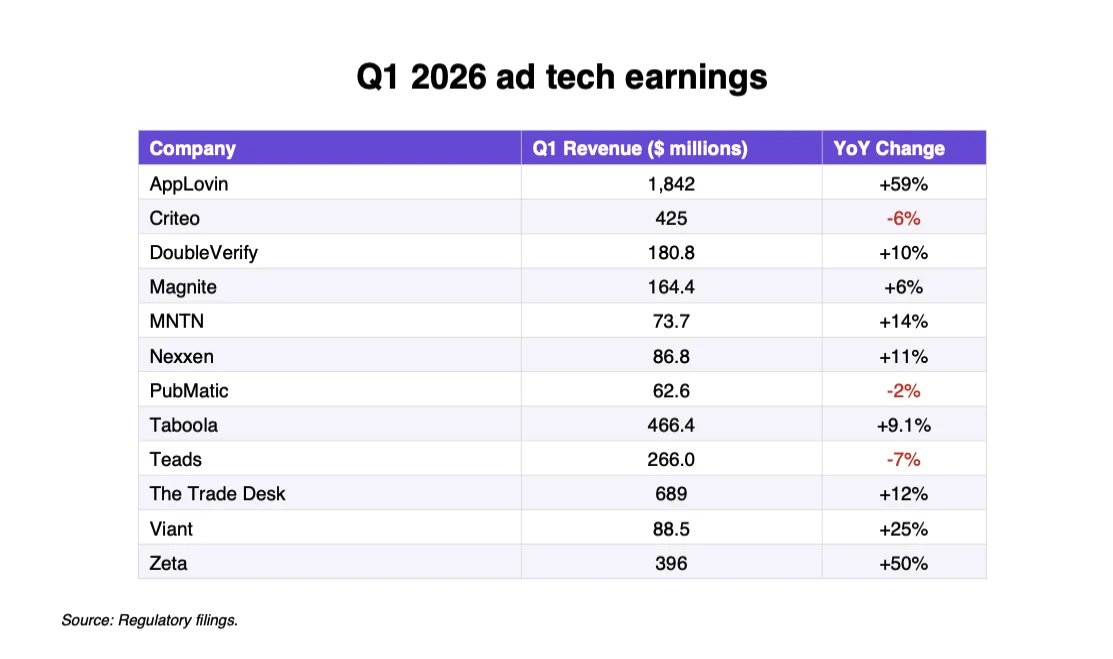

The Q1 reporting period for a cohort of 12 major ad tech players revealed a market characterized by resilience but shadowed by anxiety. While the majority of these firms reported revenue increases, the narrative was far from universally positive. Three major players posted year-over-year revenue declines, casting a pall over the industry’s broader claims of AI-driven optimization.

The dominant headline was the continued ascent of AppLovin, which generated nearly $2 billion in the first quarter—a figure that underscores the power of scaled, performance-driven advertising. However, even these impressive figures are dwarfed by the AI-fueled revenue explosions seen in Big Tech. For the ad tech cohort, the challenge is not just growth, but proving that their platforms possess the "stickiness" required to survive in an era where AI agents might soon automate the very workflows they facilitate.

Chronology of the Quarter: Trends and Turning Points

The earnings cycle, which concluded in early May, served as a litmus test for how different firms are navigating the transition from traditional programmatic advertising to AI-integrated ecosystems.

- Early May: The Trade Desk’s earnings call on May 7 sent shockwaves through the market. Despite a strong overall presence, the company’s Q2 revenue forecast of $750 million was perceived as "soft," leading to a notable dip in its stock price. This reaction suggested that even industry leaders are not immune to the intensifying scrutiny of growth expectations.

- Mid-May: As the remaining cohort reported, a pattern emerged. Companies like Criteo and Teads struggled to maintain momentum, with Criteo reporting a 6% revenue slump, largely attributed to a lag in retail media spend. Meanwhile, the market began to digest the implications of "agentic" business models—a buzzword that dominated executive commentary but left analysts questioning the long-term impact on platform reliance.

Supporting Data: Where the Money is Moving

The data from Q1 2026 highlights a definitive shift in capital allocation, specifically regarding Connected TV (CTV) and the integration of AI tools.

The Rise of CTV

CTV has emerged as the unequivocal high-quality growth segment on the open internet. The data is compelling:

- Viant: CTV ad revenue now accounts for more than 50% of total spend on its platform, a shift that likely motivated its strategic acquisition of TVision.

- The Trade Desk: Online video, including CTV, now represents over half of the total spend across the platform.

- Magnite: Executives cited CTV as the primary driver of the company’s business, confirming its status as the most vital inventory source in the current landscape.

- MNTN: While seeing a notable uptick in small-to-medium business (SMB) adoption for CTV buys, there is a looming threat that this growth rate may decelerate as giants like Meta and Pinterest expand their own CTV offerings.

The AI Implementation Gap

While executives were eager to highlight AI integrations, concrete examples of "AI-generated revenue" remain scarce.

- PubMatic claimed over 1,000 AI-powered deals.

- Taboola pushed its "AI Answer engine" as a core growth pillar for publishers.

- Criteo highlighted its OpenAI partnership, though it indicated that specific revenue guidance regarding this venture would not be available until next year.

Official Responses and Executive Strategy

The response from the C-suite to these market pressures has been largely defensive, characterized by a "glass-half-full" interpretation of AI labor displacement.

When questioned by analysts about whether self-serve AI workflows would reduce the operational dependence of agencies—thereby compressing take-rates—executives largely pushed back. There is a concerted effort to frame AI not as a threat to current business models, but as an efficiency tool. However, the tension remains palpable.

For instance, the merger between Teads and Outbrain continues to face scrutiny. A year after the announcement, the market is still questioning the investment thesis of pairing performance-driven wares with premium potential. With Teads reporting a 7% year-over-year revenue decline, analysts are openly asking if AI is eroding the historical distinction between upper-funnel brand awareness and lower-funnel performance media.

Implications: Consolidation and Margin Control

The most profound takeaway from the Q1 reports is the growing anxiety surrounding margin control. The conflict is shifting from a battle for transparency to a battle for the bottom line.

The Shrinking Addressable Market

There is a growing perception that the addressable market for independent ad tech is tightening. Disputes over margin control—whether involving agency holding companies or the traditional friction between supply-side platforms (SSPs) like Magnite and PubMatic—are becoming more frequent.

PubMatic’s recent experience provides a cautionary tale: a breakdown in a relationship with a single, unnamed demand-side platform (DSP) turned what would have been a 13% revenue gain into a 2% decline. This volatility highlights the fragility of the current ecosystem.

The Harbinger of Consolidation

These dynamics have sparked widespread speculation regarding market consolidation. If AI tools continue to compress margins and if large, dominant platforms (like Meta and Pinterest) continue to encroach on niche ad tech segments, the independent sector may be forced to consolidate to survive.

The "days of bloat" appear to be over. As efficiency becomes the primary metric by which Wall Street judges the ad tech C-suite, companies that cannot demonstrate a unique, AI-defensible value proposition will likely become targets for acquisition.

Future Outlook: Q2 and Beyond

Despite the headwinds, the outlook is not entirely bleak. Half of the 12 companies in this cohort raised their forecasted revenues for either Q2 or the full year of 2026. This indicates that while the industry is undergoing a painful transition, there is still underlying demand for digital advertising.

However, the path forward is narrow. Success will likely be defined by three factors:

- CTV Dominance: Maintaining a strong foothold in the premium video space will be non-negotiable.

- AI Utility vs. Hype: Companies that move beyond "AI-slop" and demonstrate measurable ROI for their clients—rather than just "agentic" marketing speak—will command higher valuations.

- Margin Resilience: The ability to navigate agency demands for lower take-rates while maintaining profitability will determine which firms thrive and which fall by the wayside.

As we move into the second half of 2026, the industry is bracing for a period of maturation. The era of unchecked, broad-spectrum growth is being replaced by a more surgical, data-intensive, and highly competitive environment. For the independent ad tech sector, the challenge is clear: adapt to the AI-integrated reality, or be consolidated by those who already have.