In the landscape of modern Japanese consumer culture, few phenomena have experienced as meteoric a rise as oshikatsu. Translated roughly as "fandom activity," the term refers to the dedicated, often obsessive support for an oshi—a favored idol, actor, VTuber, anime character, or athlete. Once dismissed as a marginal subculture, oshikatsu has matured into a multi-trillion-yen pillar of the Japanese economy. Now, this lifestyle has achieved a new milestone of institutional legitimacy: the arrival of specialized insurance.

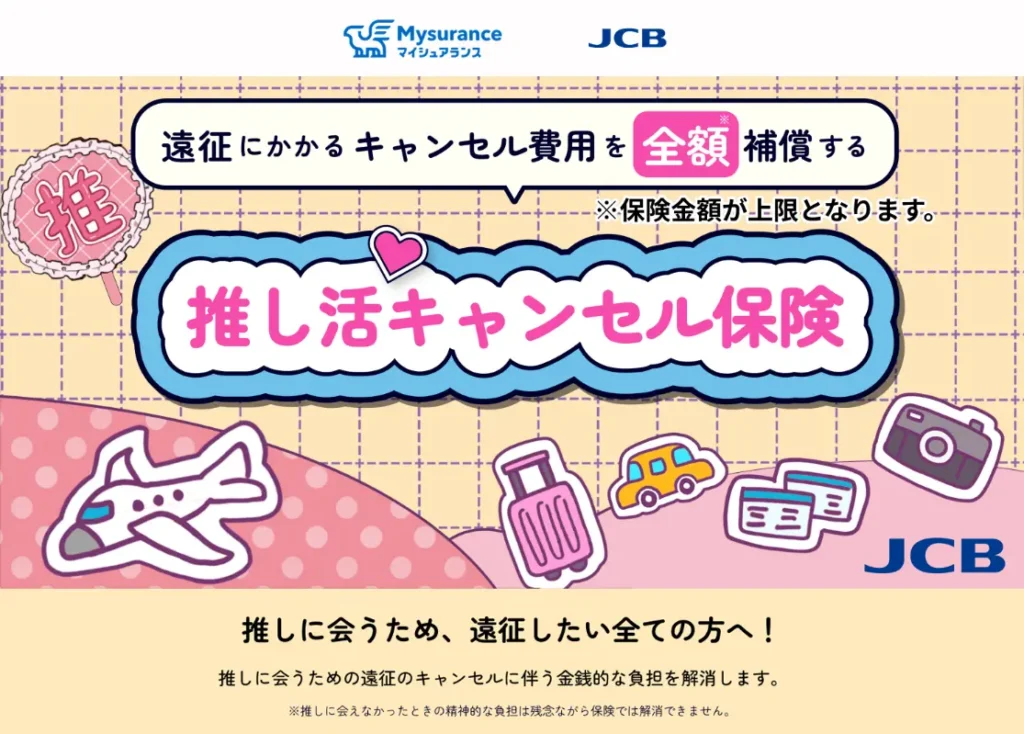

As of July 2026, Japan’s financial giant JCB has officially launched "Oshikatsu Cancellation Insurance" (Oshikatsu Kyanseru Hoken). Far from a gimmicky marketing ploy, this insurance represents a sophisticated response to the unique financial risks faced by millions of fans who treat their fandom as a primary facet of their daily existence.

The Anatomy of an Oshikatsu Trip

To understand why insurance for fans is necessary, one must understand the culture of ensei. In the world of oshikatsu, fans do not simply watch a concert from their living rooms. They travel.

Ensei refers to the pilgrimages fans take, often across the country, to attend live events, stage performances, or pop-up cafe collaborations. These journeys are expensive and logistically complex, involving bullet train tickets, flights, and pre-booked accommodation. For many, these trips are the culmination of months of saving and the grueling process of winning highly competitive, randomized ticket lotteries.

When a concert is canceled due to a performer’s illness, a typhoon, or sudden technical issues, the loss for the fan is twofold. They lose the "emotional payoff" of seeing their idol, and they lose the sunk costs of their travel arrangements. Previously, these costs were simply written off as bad luck. JCB’s new insurance policy effectively transfers that financial risk away from the individual, acknowledging that for a significant portion of the Japanese population, these trips are not optional luxuries, but essential life events.

A Chronology of Institutional Recognition

The path to this specialized insurance was not overnight. It required a shift in how corporations perceived the otaku demographic.

- April 2025: Mysurance, a micro-insurance subsidiary of Sompo Japan, launched the first iteration of the "Oshikatsu Cancellation Insurance" in partnership with the fan-focused platform Oshicoco. This initial launch was designed to test the market, relying on direct engagement with fan communities.

- Late 2025 – Early 2026: Following the launch, the product gained significant traction, winning the 2025 Good Design Award and the Shogakukan DIME Trend Award. These accolades signaled to the broader corporate world that fan-centric products were not only viable but highly prestigious.

- July 7, 2026: JCB, one of Japan’s most prominent credit card issuers, formally entered the space. By integrating the insurance into its existing digital ecosystem—specifically its cardholder app—JCB transformed a niche product into a mainstream consumer service.

This timeline reflects a broader "mainstreaming" of otaku culture. What began as a grassroots effort to protect fans has evolved into a strategic financial product offered by one of the nation’s most established credit institutions.

The Economic Data Behind the Policy

The decision to launch this product was not based on sentiment, but on rigorous market research. Mysurance conducted extensive surveys of frequent ensei travelers to map out the frequency and cost of travel cancellations.

The data revealed that approximately one in five oshikatsu participants had been forced to cancel a trip at least once. Of those individuals, roughly one-third reported losing over ¥30,000 (approx. $185 USD) in non-refundable travel expenses. When scaled against the total number of people participating in oshikatsu—which has nearly doubled from 11 million in 2024 to nearly 20 million in 2026—the financial exposure for the average fan becomes staggering.

According to the Japanese Ministry of Finance and independent market analysis from entities like Oshicoco, the oshikatsu market now commands an estimated share of ¥4.1 trillion (roughly $25 billion USD). The spending habits are consistent and high-frequency: domestic idol fans spend an average of ¥48,000 annually, while music and K-pop enthusiasts spend between ¥27,000 and ¥34,000. These figures account for travel, merchandise, and membership fees, proving that the fan economy is a resilient and growing engine of domestic consumption.

The Policy Framework: What is Covered?

The policy, while comprehensive, is designed with specific guardrails to maintain fiscal viability.

- Coverage Scope: The insurance reimburses cancellation fees for transportation (trains, flights) and accommodation. It covers scenarios such as event cancellations, significant public transport delays, and sudden medical emergencies involving the policyholder or an immediate family member.

- The Ticket Exclusion: Crucially, the insurance does not cover the cost of the event ticket itself unless that ticket was bundled into a larger travel package. This is a deliberate design choice, as the secondary market for tickets is highly regulated in Japan, and insuring the tickets themselves would invite fraud.

- Exclusions: The policy does not trigger if a fan simply decides they no longer want to go, or if their "favorite" member of a group is absent while the event still proceeds. This ensures the policy remains an "insurance" product rather than a "guarantee of satisfaction."

The pricing is designed to be accessible. For a trip valued at ¥30,000, the premium is a mere ¥900 ($5.50). This low barrier to entry is essential for the demographic, which includes many young people and students who might otherwise be unable to afford traditional, high-premium travel insurance.

Redefining Financial Literacy for Fans

Perhaps the most innovative aspect of this product is its communication strategy. Mysurance recognized that traditional insurance contracts, laden with dense legal jargon, would alienate their target audience.

Instead, the company engaged in a total rebrand of the "insurance experience." They utilized four-panel manga, testimonials from fans who had actually faced cancellation nightmares, and plain-language guides that mirrored the aesthetic of fan-made zines. By speaking the "language of the fandom," Mysurance achieved a level of trust that traditional financial institutions usually struggle to cultivate. This approach was central to their success in winning the 12th Micro-Insurance Award, as it demonstrated that financial literacy can be taught effectively when it is contextualized within a user’s passion.

Future Implications: The "Oshikatsu" Standard

The success of this insurance policy carries profound implications for the Japanese economy and the future of consumer engagement.

First, it validates the oshikatsu lifestyle as a legitimate economic activity. When a major credit card company creates a policy specifically for this demographic, it signals to other industries—such as banking, real estate, and hospitality—that "fandom" is a reliable metric for market segmentation.

Second, it sets a precedent for "lifestyle-specific insurance." We are entering an era where insurance products are becoming increasingly granular, moving away from broad "travel insurance" toward coverage that understands the purpose of the travel. This micro-segmentation allows for cheaper premiums and higher relevance for the consumer.

Finally, the policy provides a psychological safety net. By mitigating the fear of losing money on a canceled trip, JCB and Mysurance are effectively encouraging more fans to travel further and more often. This likely creates a virtuous cycle: increased confidence in travel leads to more attendance at regional events, which stimulates local economies across Japan, beyond the traditional hubs of Tokyo and Osaka.

As the lines between personal identity and consumer identity continue to blur, the oshikatsu movement is leading the way. What was once considered a hobby has become a lifestyle, and now, thanks to the foresight of companies like JCB, that lifestyle is protected by the full weight of the financial system. For the modern Japanese fan, the peace of mind offered by a ¥900 policy is more than just good business—it is the ultimate sign that their devotion is valued, understood, and finally, taken seriously.